The report offers market size and forecasts in terms of Value(USD million) for all the above segments.

Market Snapshot

| Study Period: | 2017-2027 |

| Base Year: | 2021 |

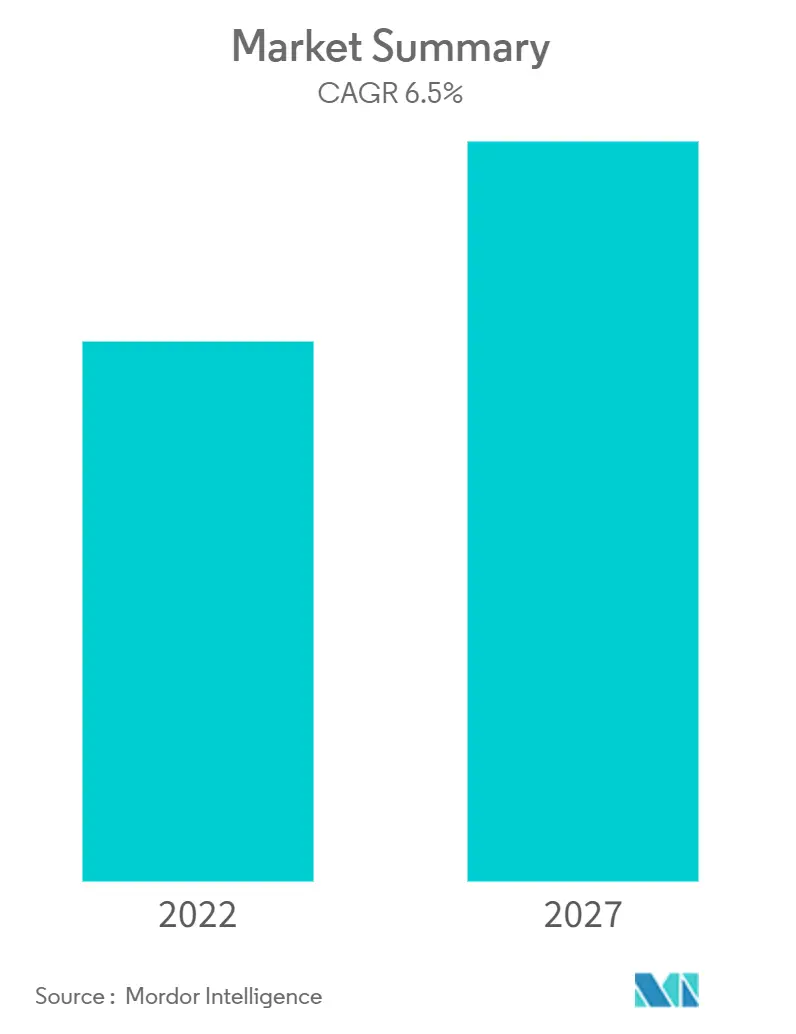

| CAGR: | 6.5 % |

|

User Rating: 5 / 5

| Study Period: | 2017-2027 |

| Base Year: | 2021 |

| CAGR: | 6.5 % |

|

The African agricultural machinery market is projected to register a CAGR of 6.5% during the forecast period(2022-2027).

The restrictions imposed due to COVID-19 have negatively impacted the global economy. According to the companies, their supplier's and distributors' business was also affected due to challenges in supply as a result of the COVID-19 pandemic. The COVID-19 pandemic has further intensified the need for agricultural mechanization, with shrinking local labor markets, movement restrictions of migrant and rural labor essential for farming, and negative impacts on overall food supply chains.

over the years, agricultural mechanization has become an integral component of agricultural development in the rest of the African countries, resulting in the evolution of agricultural machinery hire services. The expansion of agricultural productivity through increased investment into the segment for farm mechanization by the government has increased the adoption of autonomous agricultural machinery. The tractor is directed remotely by directing it into areas of the farm that have already been mapped. This enhances the accessibility and convenience of producers and directly improves the yield.

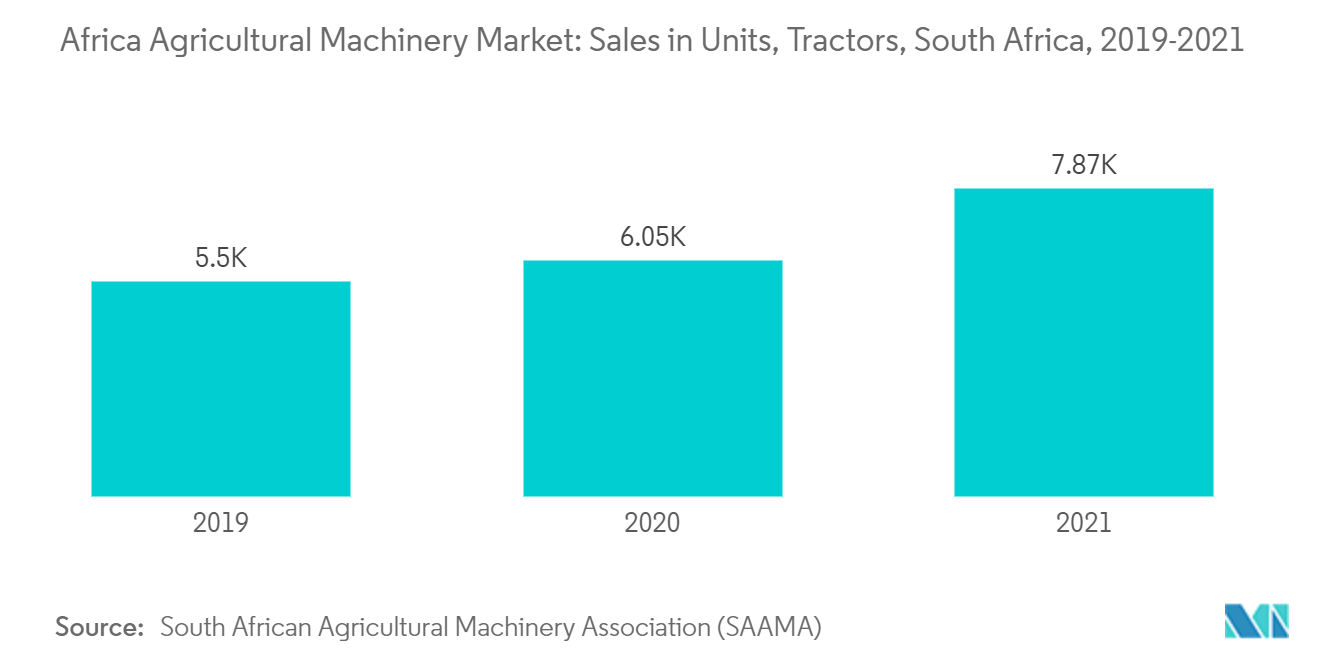

Tractors dominated the agricultural machinery market. According to the South African Agricultural Machinery Association (SAAMA), in August 2021, tractor sales of 724 units were almost 56% more than the 465 units sold in August 2020. Year-to-date tractor sales are almost 30% up on last year. 14 combine harvesters were sold in August 2021, which is one unit more than the 13 units sold in August 2021. On a year-to-date basis, combined harvester sales are almost 25% up on last year. Individual ownership, collective ownership, fee-based service delivery, and leasing are the types of machinery usage systems followed in the region.

For the scope of this report, agricultural machinery includes machines used on fields like harvesting machinery, haying and forage machinery, irrigation machinery, and other types, which are considered in the research scope. The report defines the market in terms of end-users, who procure machinery for applications in agricultural production, only. The end-users include farmers and institutional buyers, operating in agriculture, and allied production.\

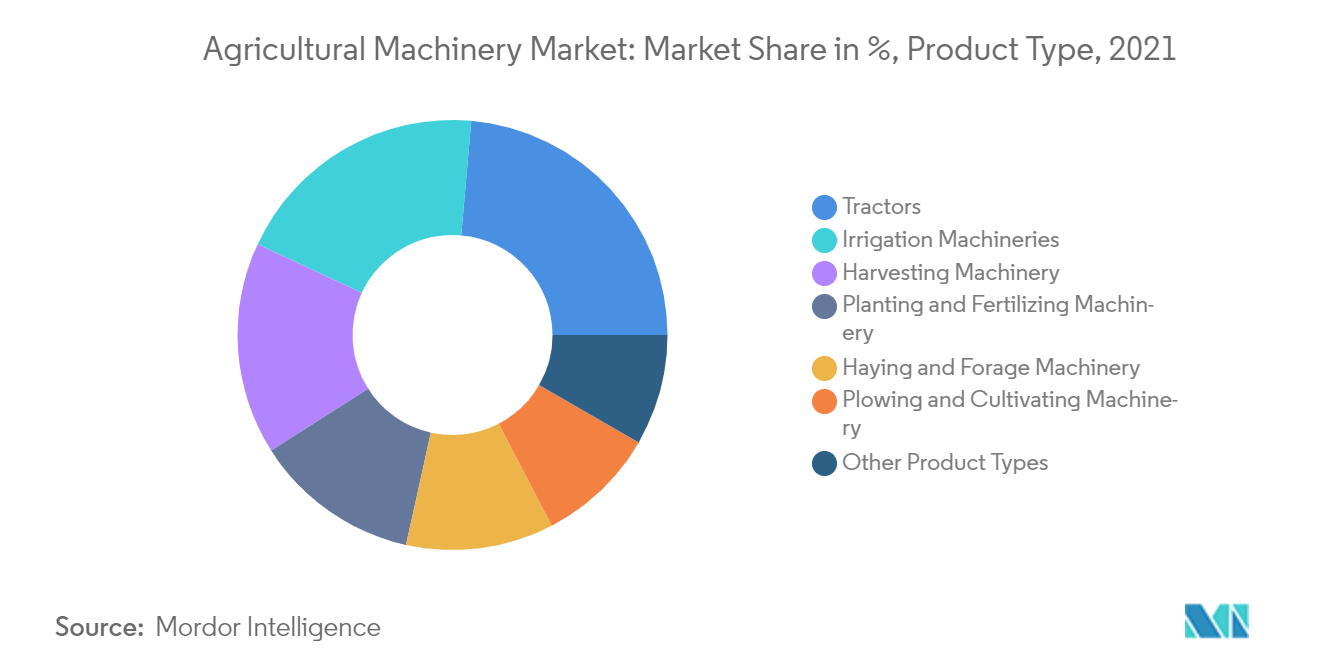

Africa Agricultural Machinery Market is segmented by Type (Tractors, Plowing and Cultivating Machinery, Planting and Fertilizing Machinery, Harvesting Machinery, Haying and Forage Machinery, Irrigation Machinery, and Other Product Type), and by Geography(South Africa and Rest of Africa). The report offers market size and forecasts in terms of Value(USD million) for all the above segments.

Agriculture plays a crucial role in Africa's economic development, but the sector is performing below its potential. Currently, around 60% of Africa's population depends on agriculture for livelihood, yet the sectorial contribution to the gross domestic product was paltry 21% in 2017. Even though Africa has the highest area of uncultivated arable land in the world, its productivity lags far behind other developing regions. Moreover, crop yields are only reaching 56% of the international average. So, there is a dire need to increase crop yields in the coming decades to keep pace with food demand driven by population growth and rapid urbanization in Africa. Therefore, the mechanization can, directly and indirectly, bridge the yield gap, by reducing the harvest and the post-harvest losses. According to the Food and Agriculture Organization of the United Nations (FAO), agricultural mechanization in Africa is still at its initial stages. FAO undertook the studies and revealed that mechanization in the country is slowly moving from hand-driven technology to power sources. For instance, as of 2017, Central Africa had 15% of its land entirely under power sources, followed by West, Southern, and Eastern Africa, with 30%, 46%, and 50%, respectively. As a result, the availability of tractors per hectare in the Southern African Development Community(SADC) has risen. However, as stated in the sustainable development goals, indicated in agenda 2063, the African Union Commission(AUC), and the Food and Agriculture Organization of the United Nations (FAO) view agricultural mechanization as an immediate indispensable action attaining the Zero Hunger vision by 2025. Such initiatives towards sustainable agricultural mechanization are likely to boost the market for agricultural machinery and implements shortly.

To understand key trends, Download Sample Report

The African tractors market was valued at USD 1.21 billion in 2019 and is anticipated to witness a CAGR of 9.6% during the forecast period. According to the research survey conducted by Agri evolution Alliance, Africa holds a great market potential for agricultural machines, including tractors in particular. The government's increasing support to develop this market is estimated to drive this sector. For instance, the government in Ghana provides tractors at subsidized rates to entrepreneurs who run 89 centers that rent out, and service tractors. In major parts of Africa, tractor sales were affected due to uncertainty regarding crop yields and exchange rates.

Robust tractors sales suggest optimism about the 2020/21 summer crop season

Robust tractors sales suggest optimism about the 2020/21 summer crop season

Additionally, issues concerning land restitution and farmworkers' shares in farms added to the farmers' uncertain conditions. According to the South Africa Agricultural Machinery Association, the sales of tractors in 2018 increased by 10.4% compared to 2017. The sales of tractors were 3,930 units by July in 2018, as compared to 3,557 units by July in 2017. However, currently, the region is facing major constraints, which hampers its growth in this market. One such limitation is the private sector's involvement that is severely hampered by government resistance and corruption, affecting the imports of tractors.

To understand geography trends, Download Sample Report

In the African agricultural machinery market, companies are not only competing based on equipment quality and promotion. Still, they are also focused on strategic moves to hold larger market shares. New product launches, partnerships, and acquisitions are the major strategies adopted by the leading companies. International players dominate the market. These players accounted for 80% of the market in 2020. Some of the key players in the market are Deere and Company, Kverneland AS and CNH Industrial N.V

AGCO in April 2021, expanded its market presence in the African continent, by launching its first Fendt dealers in South Africa. This was an essential phase in AGCO’s New Way Forward strategy to draw closer to customers in the region and acquire market share.

In 2021, John Deere has introduced 2 new series of tractors that have the farming community abuzz. The product includes 6B and 5D series.

In 2020, Deere & Co. is teamed up with the Hello Tractors company in Africa. Startup Hello Tractor’s technology allows farmers to hail the machines via an app, monitor the vehicles’ movements, and transmit usage information such as fuel levels.

We do have a lot of videos related to farming machinery in South Africa- most of them are very unprofessional and some of them are branded in the name of the production company and also not our standard.

![]()

![]()